Why Turkish Banking Sector?

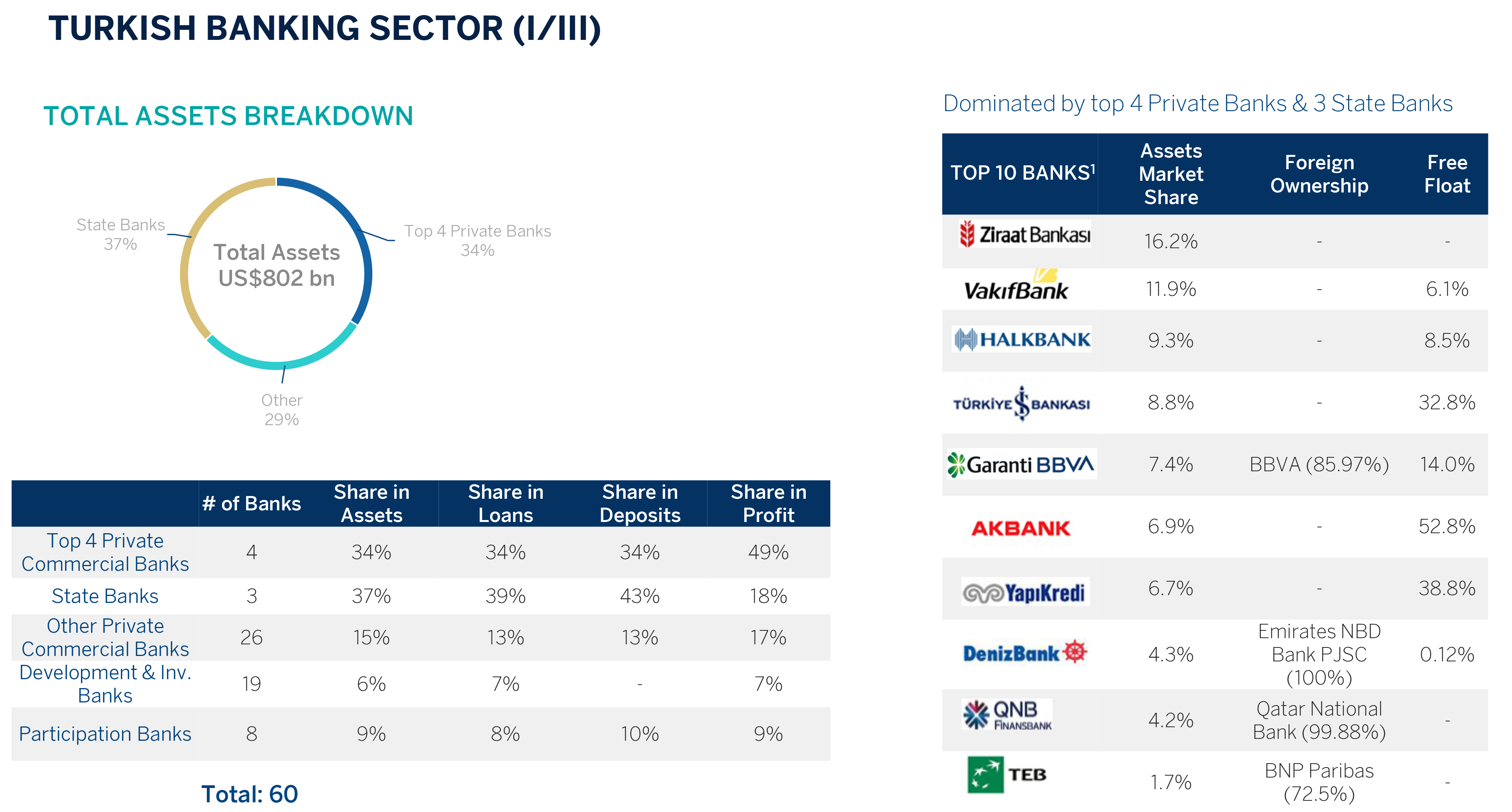

TURKISH BANKING SECTOR

Note: Sector figures are based on bank-only BRSA monthly data as of December 2023. Banks owned by SDIF are not listed above

1 Top 10 banks make up ~80% of sector’s total asset as of Dec-23.

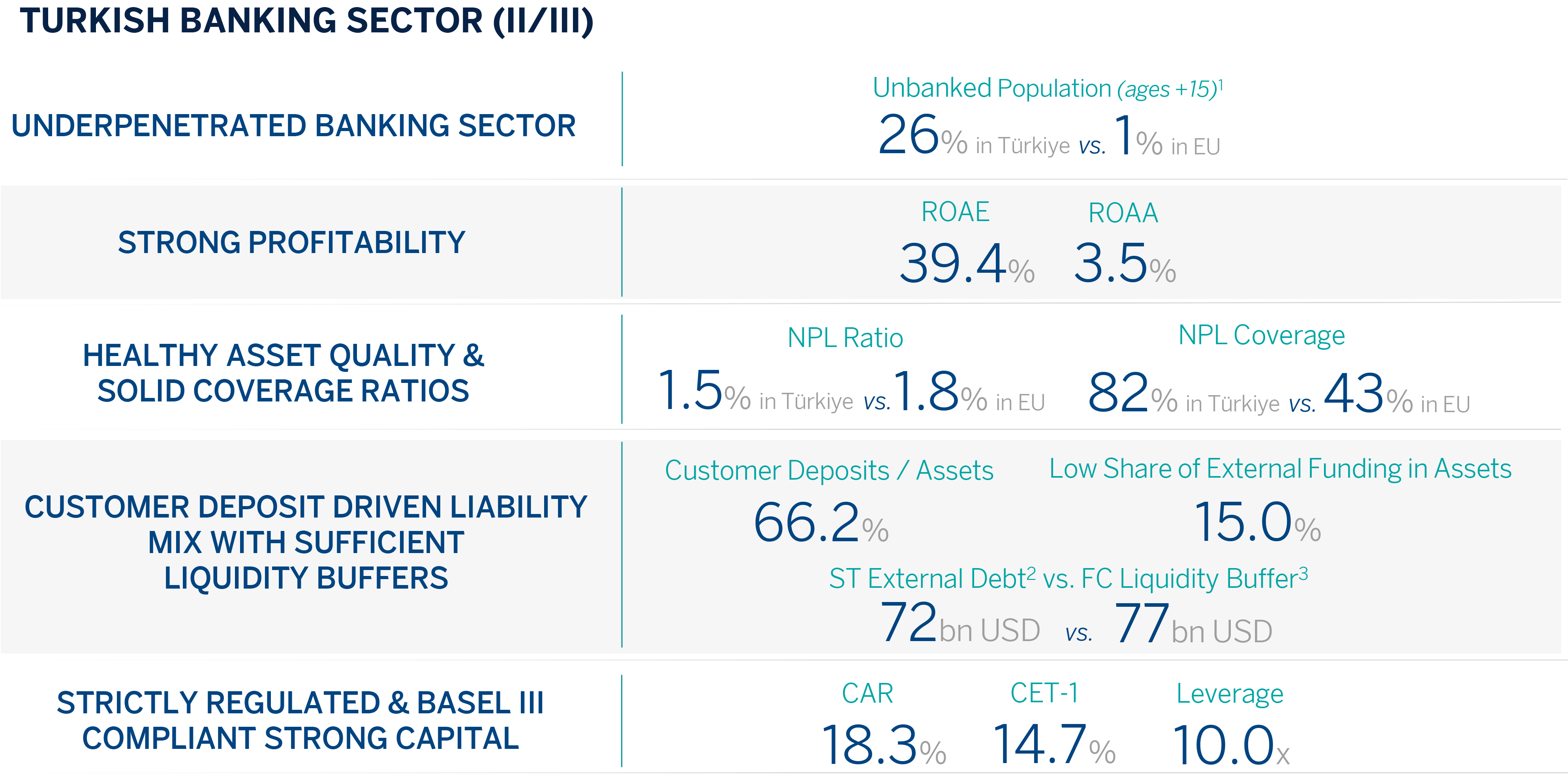

Note: Commercial banks’ figures are based on BRSA monthly data as of December2023. Leverage defined as Debt / Equity

(1)Based on having an account in a financial instution.

(2) CBRT, as of December. Excludes non-residents’ FC deposits

(3) Quick Liquidity Buffers: FC reserves Under ROM, swaps, money market placements, CBRT eligible unencumbered securities, cash, FC collateral deposit

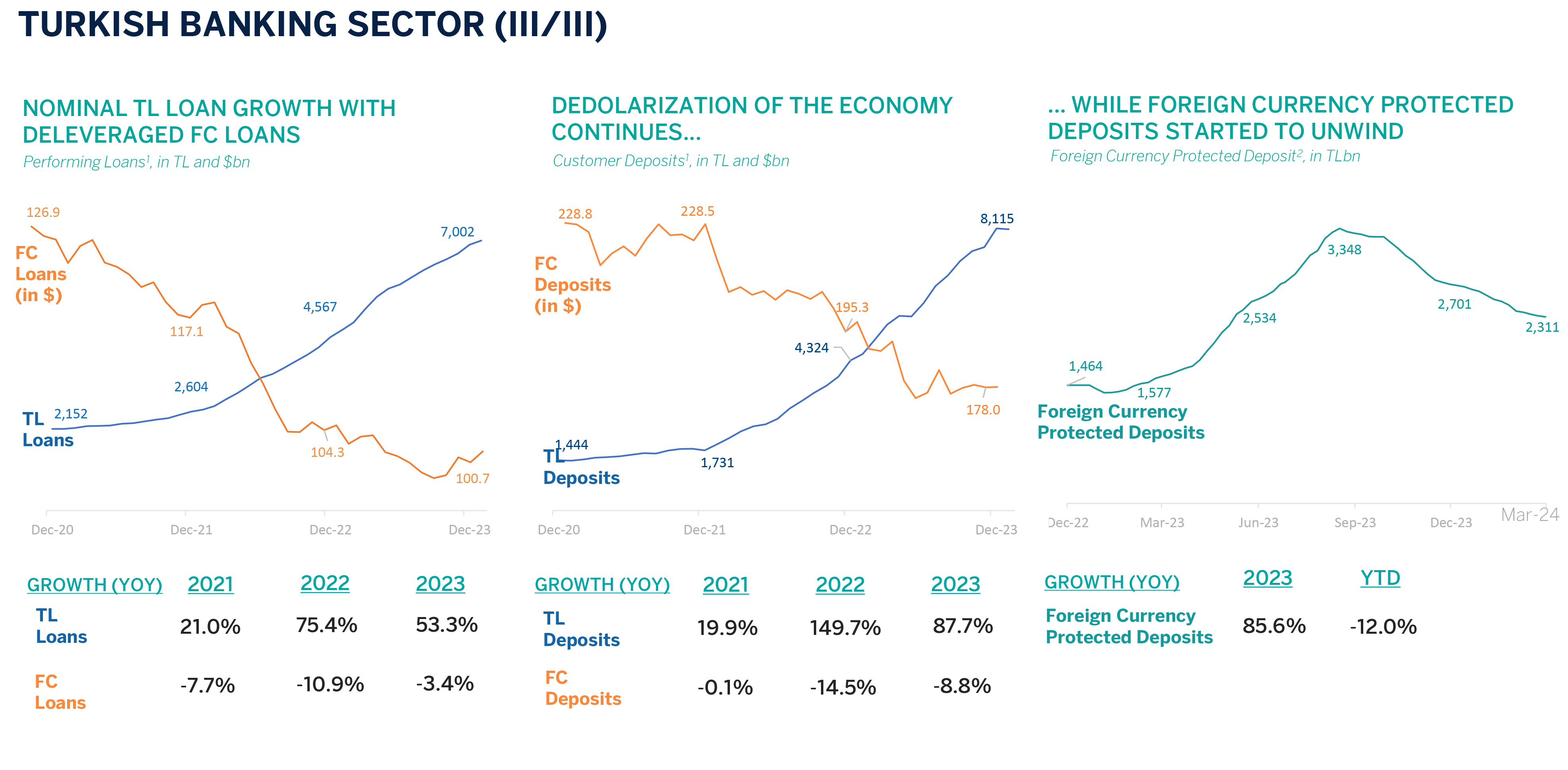

1 Based on BRSA monthly data as of December 2023, for commercial banks only.

2 Based on BRSA weekly data as of 01 March 2024, for the sector.