Market Recap

Synchronous economic growth across the globe continued with supportive fiscal prospects and easy financial conditions. In the last quarter of the year, MSCI World rose 5% capping off a solid yearly growth with 20% YoY. Global equities ended 2017 on a high note. Upwards earnings revisions in 2017 was a contrast to the flattish or modest downward revisions seen in the last five years.

Economic fundamentals have improved broadly across Europe and other parts of the developed world. As it did throughout most of 2017, Euro continued to strengthen against the Dollar during the quarter. This was attributed to the ECB policy and better-than-expected European growth. Profit-taking and a strong euro were factors in MSCI EM index receding 0.5% in 4Q. Political events in Spain and Germany also weighed-in on the markets. In the US, S&P 500 rose 6.6% in the last quarter. Robust corporate earnings from the consumer discretionary sector, technology sector and financials also helped overall sentiment. Equity markets were buoyed by the US Tax law, which reduced the highest corporate tax rate from 35% to 20%. Generally positive macroeconomic data also supported the markets, such as the better-than-expected third-quarter annualized GDP growth of 3.0% in the US. Another important indicator is the all-time low volatility in developed equity markets. Daily S&P 500 Index volatility hovered near its first historic lows for most of 2017, which reflected the strong macro backdrop. As expected, FED lifted interest rates by 25bps in December, and raised its growth forecasts for 2018 to 2.5% from 2.1%.

On the commodities front, Brent crude rallied another 18% on top of its 20% QoQ increase in the previous quarter. On top of increasing global demand; an agreement among OPEC, and a number of non-member countries such as Russia, to extend production cuts to the end of 2018 helped oil prices. As Chinese demand remained firm industrial metals rose.

In 4Q EMs experienced strong foreign funds inflow from the equity and the bond markets in the amounts of US$ 18.8 billion and US$ 11.3 billion, respectively, according to IIF data. As a result, MSCI EM rose 7%, and recorded a 34% YoY growth. Political developments supported gains in EMs. In South Africa, Ramaphosa was elected leader of the African National Congress, which increased the prospect for a return to more orthodox policy after elections in 2019. Greek equities rallied as the country reached agreement with international creditors over reforms, paving the way for the dispersal of further bailout funds. India outperformed as the government announced plans for a major recapitalization for state-controlled banks. In contrast, Mexico posted a negative return, attributable to peso weakness, amid concerns on NAFTA modernization negotiations.

In 4Q17, MSCI Turkey rose 4% and underperformed MSCI EM by 3%. Nevertheless, on a yearly basis MSCI Turkey performed in line with MSCI EM. According to the monthly BIST foreign transactions data, Turkish equites attracted US$1.8bn of foreign investments in 2017. In December Turkey attracted US$180mn worth of foreign investments, despite outflows worth US$192mn in the prior two months. Global risk appetite, combined with domestic inflation outlook and local politics resulted in strong lira depreciation in the second half of November, the exchange rate rose to an all-time high at 3.96 TRYUSD. Lira depreciated by 9.8% QoQ against Dollar, however, yearly depreciation was limited to 7.5%. The Benchmark interest rate touched 14.34% in the second half of November, highest level since March 2009, and ended the quarter at 13.40% registering 151bps increase QoQ.

Looking ahead, markets expect the positive momentum to continue. Growth should endure as more developed and emerging market countries participate. Yet, the pace of the recovery most likely peaked in 2017. Equities made considerable gains in 2017 and reached their full valuations. Earnings growth will be the primary driver going forward. Central banks entered an era of policy transition, with rate and balance sheet normalizations, however they will remain accommodative.

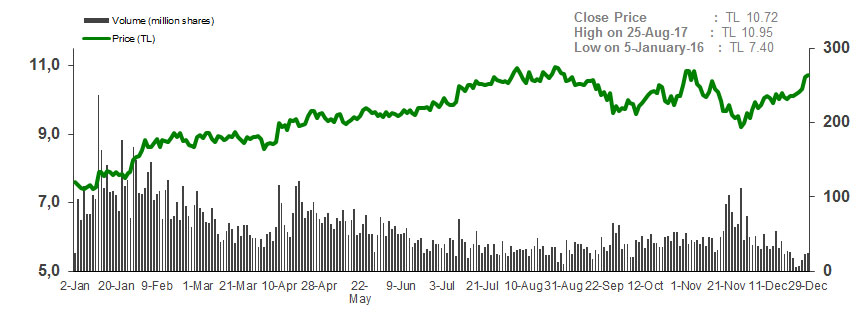

Garanti BBVA Stock Performance in 2017

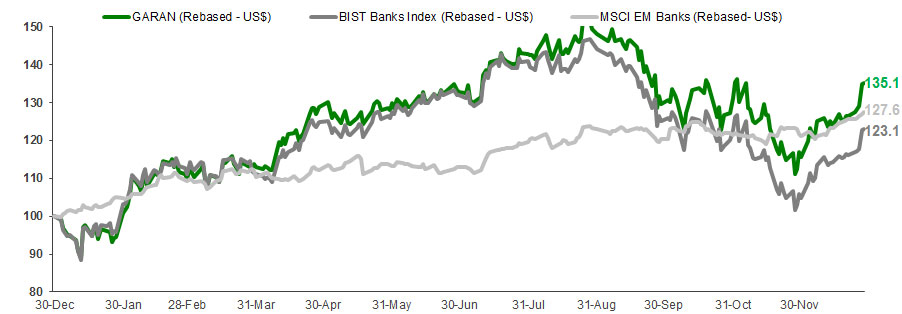

Relative Performance to MSCI EM Banks & BIST Banks Index

| Brazil |

-3% |

21% |

| China |

8% |

51% |

| Hungary |

7% |

37% |

| India |

12% |

37% |

| Mexico |

-9% |

14% |

| Poland |

6% |

52% |

| Russia |

3% |

0% |

| Turkey |

4% |

34% |

| EM |

7% |

34% |

| EMEA |

11% |

3% |

| EM Banks |

6% |

28% |

| Eastern Europe |

4% |

13% |

| Latin America |

-3% |

21% |